When Liz Truss and Kwasi Kwarteng’s tax-cutting mini-budget triggered a UK debt crisis in autumn 2022, the pound plummeted to almost parity with the US dollar. In 2023 the UK has endured weak growth, falling productivity and high inflation, yet the pound has been the strongest performing currency among the G10 leading economies. It is currently trading at almost US$1.31, its highest level since April 2022.

To help understand what’s going on and where the pound goes from here, we spoke to Ganesh Vishwanath-Natraj, assistant professor of finance at the University of Warwick.

Many thought last autumn that the pound would keep falling to dollar parity and below. What changed?

The Bank of England’s interest rate tightening is probably the key factor. Though also the government’s fiscal policy has been more restrained.

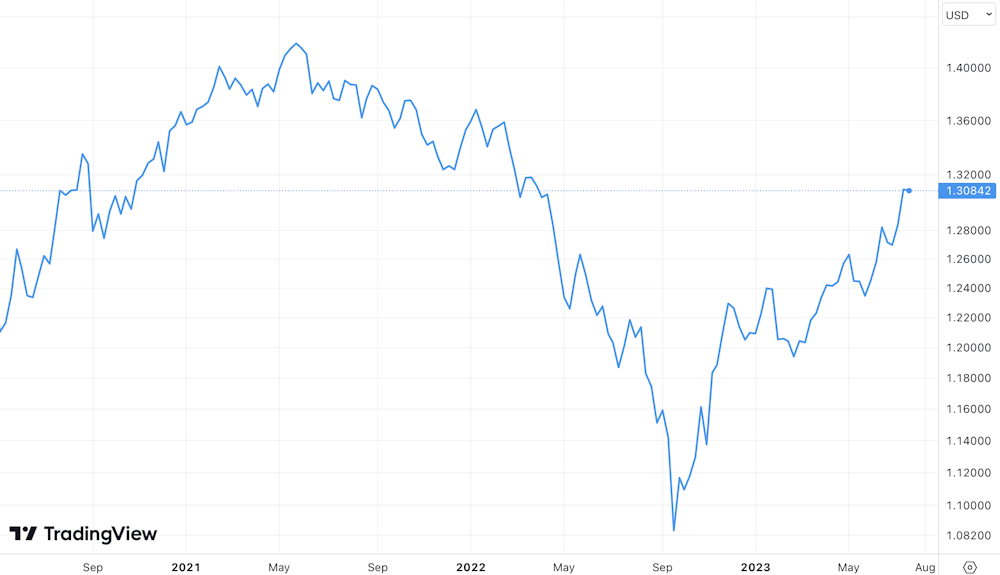

Pound v US dollar 2021-23

{kind=link}

Trading View

But interest rates have been tightened in many countries. Why would it have made such a difference in the UK?

If you compare them to the US, for example, the federal funding rate has risen from basically 3% to 5% since last October. The equivalent UK rate has gone up from just over 2% to 5%. Not only has the UK tightened more, the markets expect the Bank of England to keep tightening.

One reason for the stronger pound is that the US dollar has weakened over the same period. This may account for 50% of the change in the pound. Yet the pound has also gained against other currencies like the euro (rising from about €1.08 to €1.17 over the same period). This suggests that the pound’s appreciation is more likely due to UK policies than foreign factors.

Why has the US dollar been losing value?

The dollar is often seen as a measure of risk appetite – in other words, when the dollar is strong, there’s more pessimism in the global economy. The VIX index is evidence for this: it is a measure of how much fear is in the market. Since October, it has fallen from about 32 to 14.

The US dollar over time

Trading View

The whole de-dollarisation narrative may also be having an effect. This is the idea that the dollar’s status as the world reserve currency is eroding because countries like China, Russia and Saudi Arabia have been turning away from the US currency. This is probably more of a long-term issue, but it may still be encouraging investors to short the dollar (bet that it will fall).

One other thing to note is that the falling dollar goes against inflation expectations. US inflation has been falling faster than in other countries, which all things being equal should cause the dollar to rise.

UK ten-year gilt yields are now higher than last autumn. Doesn’t that suggest sentiment about the UK has got worse?

The spike in gilt yields in autumn 2022 reflected investor panic after the mini-budget [gilts are bonds issued by the UK government to borrow money – the yields are the interest paid on the bonds; the higher the yields the lower the demand for the debt]. Yields fell back down to about 3% after the change of fiscal policy once Rishi Sunak became prime minister, which was probably the “correct” level for where interest rates were at the time. The rise in gilt yields since then reflects the rises in interest rates.

UK 10-year gilt yields

Trading View

Is it unusual to see a currency strengthening so much when the economy is weak?

High inflation and rising government debt would normally be associated with a weakening currency, so the rising pound is not a reflection of UK fundamentals. It could reflect the fact that investors are expecting UK inflation to fall quickly, but that’s not what forecasts are saying. For example, NIESR (The National Institute of Economic and Social Research) thinks that inflation won’t return to 2% levels until 2025.

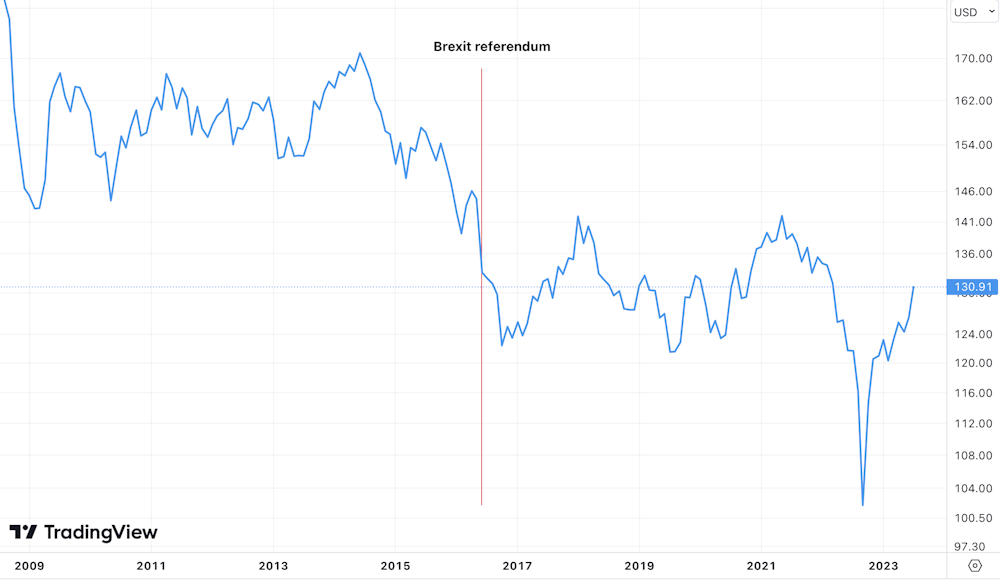

Many thought Brexit helped to cause the pound’s 2022 crash. Does the pound’s appreciation reflect investors feeling more optimistic about Brexit?

Probably the effects of Brexit on the pound were seen more in the one-off fall in 2016 after the referendum. The pound has never recovered to pre-Brexit levels.

The pound’s performance over time

Trading View

Who will win and lose from a stronger pound?

The winners will include consumers of imports and those travelling abroad, particularly to the US. Firms that buy goods in dollars will be benefiting. On the other hand, exporters are losing out.

Is it good news overall?

I would say so, yes. In general, it means that investor sentiment on the UK economy has improved and the gilt market has stabilised. It means there are net inflows into the UK economy (meaning more money is coming in than going out).

Where does the pound go from here?

I always pay attention to The Economist’s Big Mac Index, which gives a sense of the relative value of different currencies by comparing the price of a McDonald’s Big Mac around the world. When last published in January, it suggested the pound was 12% undervalued against the US dollar. The new index is due any time now, and will probably show that this undershoot has been corrected.

The question is whether the pound now keeps rising towards the sort of US$1.50 levels we used to see before Brexit. I think it’s likely that we will head in this direction. Brexit was in my view a one-off productivity shock in which some businesses and sectors had to react, such as by moving certain activities abroad. Now that this has happened, you would probably expect it to be offset by new industries springing up to take advantage of the new arrangement.

There has been a lot of talk about the UK positioning itself to benefit from AI and crypto, for instance. There is certainly potential there, though it’s hard at this stage to know what the impact will be.

However, a rising pound is conditional on the public finances remaining healthy and inflation falling in line with expectations. If there are issues on those fronts, particularly combined with exogenous events like a war that made the world more risk averse again, another crash in the pound would become more likely.

by : Ganesh Viswanath-Natraj, Assistant Professor, Warwick Business School, University of Warwick

Source link